|

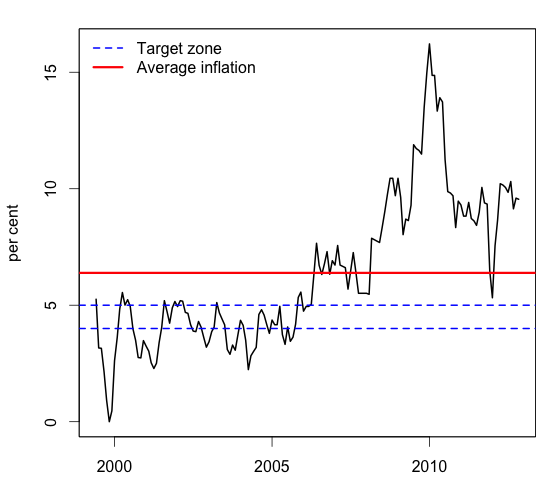

| `Headline inflation': The year-on-year change in CPI-IW, with target zone superposed. |

The best price index in India is the CPI-IW. `Headline inflation' in India corresponds to the widely watched year-on-year change in the CPI-IW. The above graph shows us the experience of inflation in India from 1999 onwards. The informal target of policy makers is for inflation to lie between four and five per cent. These are the two blue lines on the graph.

In February 2006, inflation breached the upper bound of five per cent. It has never come back in range. Things are so bad that even the overall average inflation of this period (the red line) is now above the upper bound of five per cent. We don't just occasionally fail to stay within the target range of inflation; we persistently fail to get there. This inflation crisis is a major failure in Indian macroeconomic policy, and is holding back India's growth.

Many explanations like supply side factors or droughts are offered. They fail to persuade when we see this time-series experience. Did we have fewer droughts before 2006? Or that supply side factors were not a problem before 2006? Sustained failures on inflation are always rooted in monetary policy. In the long run, inflation is always and everywhere a monetary phenomenon.

There is some tiny progress in the latest months in this graph, but we cannot claim that the inflationary spiral has been broken. Policy rates are 7 and 8 per cent, and inflation is almost surely above 8 per cent, so the policy rate is likely to be negative when expressed in real terms.

|

| Smoothed month-on-month inflation (annualised, based on seasonally adjusted CPI-IW) |

There is some progress in recent months. But at the same time, in the entire period, we see many such short periods of decline in inflation. Eyeballing the graph does not give us confidence that there has been a qualitative change in inflationary conditions. As an example, consider the previous dip in inflation. We could have become quite excited by the drop in this 3mma CPI-IW inflation down to 2%. But this was a temporary gain which was quickly reversed.

We should hence be cautious about reading too much in the recent decline in month-on-month CPI-IW inflation. While it is great news if inflationary pressures in the economy are declining, and it will be great news when the cycle of high inflationary expectations will be broken, there isn't enough evidence as yet to announce that the mission -- of achieving low and stable inflation -- has been achieved.

There are a couple of aspects that is also critical. Inflation, in India, would to a large extent be attributable to supply side problems. Policy makers have not addressed that adequately. The reality as is that political populism, like the MNERGA programs, have left a lot of money in the hands of individuals that also has to be factored. The other aspect is that conventional monetary policies do not appear to have the same impact that it used to have.

ReplyDeleteI don't think we have been following conventional monetary policies. At least, the inflation graph here seems to suggest that we haven't. Rates should have been higher during this period, given inflation. They haven't been as high, because of the supply side argument. That, in turn, has lead to reduced RBI credibility, because if the RBI governor says he can't control inflation, well, then that's how things will turn out. That is one important factor in the game of inflation expectations.

DeleteFolks wanting RBI to ease, because inflation is due to supply side problems, are making a backwards argument. Instead, they should ask the govt to enact policies that would get rid of supply side problems, thereby increasing capacity, reducing inflation and in turn, restoring the space needed for monetary policy to be effective. Lets not put the cart before the horse.

Macroeconomics is about growth (the long run stuff) and fluctuations (business cycles).

ReplyDeleteInflation happens on a business cycle scale. Supply side issues happen on the long run.

So, the argument that supply side issues are causing inflation, is wrong because the timeframes are different? That seems weird.. and counter to what we've been hearing from everybody. Surely, there are things like structurally high inflation (as opposed to based on where we are in the business cycle)?

DeleteSupply side issues are a fact but the reason for it is lack of governance. A simple example is accessibility of power supply. There is extreme shortage of power throughout the country. Electric power for mass consumption, an American invention of the late 19th century is still not implemented in India in 21st century. Monetary policy cannot help here.

ReplyDeleteA great example! Was electricity supply better in 1999-2006?

DeleteThis proves that electricity supply issues are not the source of price stability or instability.

Finally RBI cuts repo rate 25 bps....I think interest rate cycle reversal starts.....great for private sector banking stocks...

ReplyDeleteI would like to bring to your attention an issue that could be of grave concern.

ReplyDeleteI would like to point to you that currently in India, majority of the policy makers have accepted the high rate of inflation (it has been high for close to 4 years now) as they believe that the empirical data (Phillips curve) showed that in periods of high inflation, also showed a low unemployment rate. And there seems to be complete acceptance of this view in practice by the policy makers (not in words as they keep saying that their position is anti -inflationary, even though RBI governor has cited the Phillips curve various times). However in America during the late sixties and early seventies a similar debate was going on and most of the keyensian policymakers seemed to accept the philips curve. However one of the economists , Milton Friedman, predicted and argued back then that that after a sustained period of inflation, people would build expectations of future inflation into their decisions, nullifying any positive effects of inflation on employment. For example, one reason inflation may lead to higher employment is that hiring more workers becomes profitable when prices rise faster than wages. But once workers understand that the purchasing power of their wages will be eroded by inflation, they will demand higher wage settlements in advance, so that wages keep up with prices. As a result, after inflation has gone on for a while, it will no longer deliver the original boost to employment. In fact, there will be a rise in unemployment if inflation falls short of expectations. Sure enough, the historical correlation between inflation and unemployment broke down in just the way Friedman predicted: in the 1970s, as the inflation rate rose into double digits, the unemployment rate was as high or higher than in the stable-price years of the 1950s and 1960s. Inflation was eventually brought under control in the 1980s, but only after a painful period of extremely high unemployment, the worst since the Great Depression.

It was this prediction that made Friedman quite famous and ultimately was one of the reasons that he was given the Nobel prize.

However it seems that the Indian policy makers, have forgotten about the lessons of the past, and have continued with a policy of high inflation. Even the academicians, and press who usually should be very vocal about this, have shown intellectual bankruptcy and lethargy regarding this subject

I don't think so its right time to ease monetary policy. Agreed one is looking domestic factors to make such decisions which probably makes sense. For me the bigger concern when ever the next round of Quantitative Easing takes place in the US ( where US debases their currency more ), Indian central bank would continue to do the same in order to support the exporters else these exported products would look pretty expensive in US and consumers would not buy it. US has pledged to infinite QE to boost their GDP. I suspect when ever the next round of money printing takes place, inflation could spike up.

ReplyDeleteRBI's chief on concern of the inflation being still high is still valid. He seems to understand the currency wars at international markets.