|

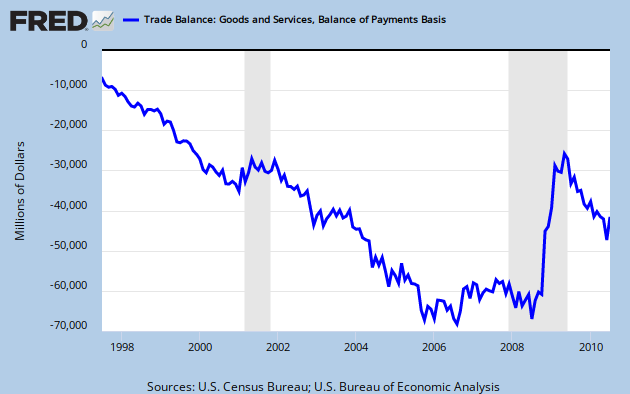

| The US trade balance (goods+services, per month, seasonally adjusted) |

Warning for Indian readers: In India, the term `trade balance' pertains only to merchandise trade. In the US, the monthly trade data covers both goods and services. So it is a meaningful measure of what is going on in international trade, unlike the corresponding Indian data.

Bretton Woods II first broke down in the financial crisis. In the downturn, the mighty American consumer purchased fewer 50" television sets. The US trade deficit dropped nicely all the way to $25 billion per month. Alongside a rise in the US savings rate, this looked like a world which was rebalancing.

In recent months, this movement reversed itself and the US trade deficit once again started getting worse. A deterioration of $20 billion per month is visible; i.e. a deterioration of $240 billion a year. Suddenly, the story of global imbalances righting themselves came under question. The present US run rate is around $40 billion a month or $0.5 trillion a year.

Alongside this, we have news that the Chinese reserves rose by $194 billion in Q3 2010. The Chinese seem to have also passed on some of their problems of exchange rate pegging upon their neighbours by purchasing Japanese, South Korean and Indonesian assets. I am not aware of such behaviour having been observed prior to this in human history. Japan, South Korea and Indonesia have taken unkindly to this behaviour. Given the opacity of the Chinese regime, one can't help wonder if similar things are going on through less visible channels - e.g. a Chinese sovereign wealth fund buys $10 billion of OTC derivatives on Nifty.

So we seem to be headed for quite some escalation of conflict over the Chinese exchange rate regime. Here are some interesting readings on the subject:

- What happens if the RMB is forced to revalue? by Michael Pettis on his blog.

- Why America is going to win the global currency battle, by Martin Wolf in the Financial Times.

- The final end of Bretton Woods 2? on Tim Duy's Fed Watch (the source of the above graph).

- The effect of RMB appreciation on the US-China trade balance, by William Thorbecke on voxEU.

- An interview with Raghuram Rajan on der Spiegel.

- Evolution of the exchange rate regime in Asia.

- How to avoid trade war: A reciprocity requirement, by Daniel Gros on voxEU, which makes a lot of sense to me as one of the least troublesome policy avenues to go down.

Very Interesting . Does US actually wants to devalue its currency now so that the Chinese imports becomes costly and BOP crisis can be reduced ?

ReplyDeleteAs of May, 2009, Beijing is the holder of treasury securities of the USA for the sum of $801,5 billion For May, 1st of this year of an investment in US Treasuries constituted 38 % of gold and exchange currency reserves of China. Chineses are interested in stable dollar from the point of view of the export. China is the largest exporter of the goods on the market of the USA. The strong dollar does the export Chinese goods by cheaper so, more competitive, therefore the government of the Peoples Republic of China is artificial supports "a weak" yuan exchange rate in relation to dollar.

ReplyDeleteGrowth of dependence of China from the American market means that Beijing won't cease in the near future buying up of debt obligations of Washington. Certainly, theoretically quite probably that Chineses take the dollar export earnings in the USA and convert them in other currencies. But it in any way won't prevent the American economy. If Chineses constrain economy of the USA, the Chinese economy also will suffer, and much more.

Hi,

ReplyDeleteCould you reduce your post per page, i am unable to read your blog on my mobile.

Raj